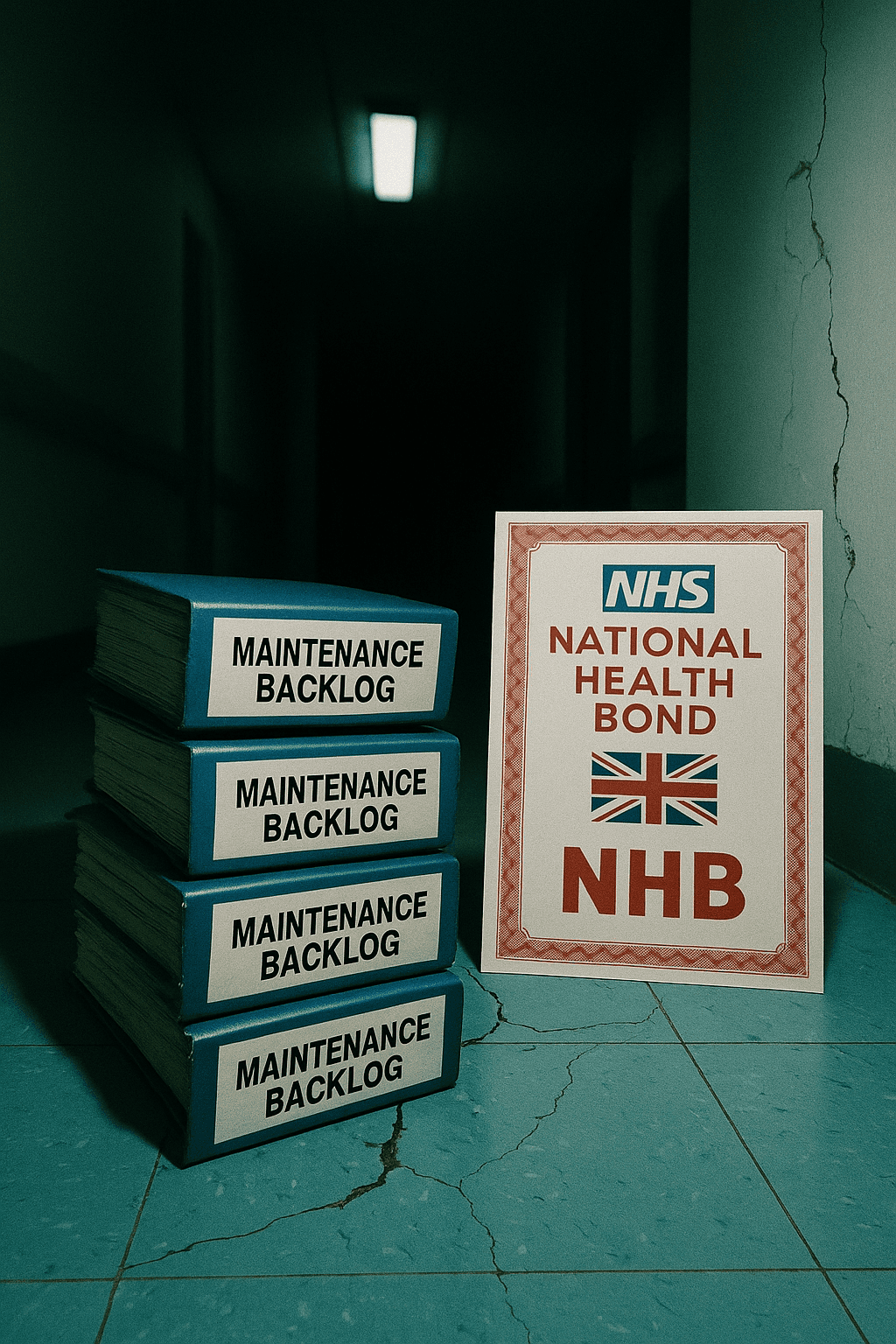

Britain’s creaking NHS can swap its £13.8 billion repair backlog for fresh scanners by letting companies pay tax in the form of hospital upgrades, not Treasury cheques.

Pressure is growing on the NHS, with outdated buildings, a mounting repair backlog, and an overstretched workforce. Hospitals face broken lifts, failing heating system,s and outdated technology with a record £13.8 billion maintenance backlog. Britain’s healthcare system is rapidly approaching breaking point. Yet, policymakers remain stuck in debates about potential funding solutions, as Amanda Pritchard, the outgoing NHS England chief, has urged ministers to reconsider private investment in healthcare infrastructure.

This poses the question of how we can secure the NHS’s future without repeating the expensive mistakes of the past.

One innovative solution is National Health Bonds (NHBs)—a financing model that is designed to attract large-scale private investment while keeping the NHS in public hands. Instead of conventional government borrowing or the discredited private finance initiatives (PFIs), NHBs would allow corporations, pension funds and individual investors to directly finance NHS infrastructure. Crucially, NHBs would provide corporate tax breaks for firms that invest and steady returns to individual investors through interest payments on the bonds issued, while ensuring that the public retains complete control of the NHS.

The UK’s corporate tax rate, now at a 15-year high of 25 per cent, has significantly reduced Britain’s attractiveness to investors, as inward investment projects have declined by nearly a third since 2016. Last year alone, foreign direct investment fell by 6 per cent. In this way, NHBs, rather than a blunt tax cut, would offer targeted tax cuts for businesses that reinvest profits directly into the UK’s healthcare system. Imagine Vodafone or AstraZeneca investing directly into improving London’s hospitals while reducing their tax burden. By purchasing NHBs, firms would directly fund urgent infrastructure improvement needs, from replacing outdated technology to repairing crumbling hospitals.

Most importantly, whilst under PFIs, the hospitals were leased back to the NHS at exorbitant costs, burdening ordinary taxpayers with billions in excessive interest and fees; under NHBs, however, hospitals will be owned by the NHS, removing the issues of inflated leasing costs. Therefore, NHBs would not duplicate the disastrous failures of previous PFIs.

A similar example is the Welsh government’s Mutual Investment Model, under which the public maintains equity capped at 20 per cent, which showcases that carefully structured private finance schemes can deliver value without excessive risk. NHBs, however, go further—completely removing private control over public assets.

Issuing bonds to pay for health care, of course, means the obligation of regular interest payments; however, this is a cost the NHS already incurs indirectly through government borrowing. Another concern is how funds will be allocated. Under the NHB model, these payments would be explicitly accounted for and transparently managed through a dedicated NHS Infrastructure Authority (NHIA) that would oversee investment allocations, regularly report how funds are spent, which hospitals are being developed, and precisely how waiting times and patient outcomes improve. The NHIA would ensure that every pound raised is directed toward projects that improve healthcare efficiency and patient outcomes, alleviating the previous concerns over PFI inefficiencies.

The current government is struggling with the competing pressures of increasing NHS funding demands and concerns over unsustainable public debt. Labour’s most recent budget has promised £25.6bn of extra funding for the NHS, taking total health spending well over £200bn by 2025/26. If the NHS were to fund itself entirely through NBHs sales, it would need approximately £214.1 billion annually to fully cover its current budget. Realistically, NHBs would initially complement rather than immediately replace government funding. However, even partial adoption could significantly reduce budgetary pressures, stimulate investment, revive confidence in Britain’s public services and improve the UK’s business conditions and attractiveness.

Sceptics may doubt that businesses are interested in engaging in public partnerships; however, institutional investors and pension funds around the globe routinely purchase and manage trillions in similar stable, long-term bonds. Therefore, why not use NHS-backed instruments? British pension funds and insurers alone have explicitly indicated a willingness to allocate up to £200 billion towards UK infrastructure projects over the next decade—if the right vehicles, such as NHBs, are available. With proven demand and invaluable returns, NHS-backed bonds would attract significant interest.

Ultimately, the Labour government faces a choice: either the NHS will adopt new ideas, like NHBs, or remain in a cycle of crisis, quick fixes, and decline. National Health Bonds provide a financially sustainable pathway forward, and policymakers and investors must act before Britain’s healthcare crisis deepens any further.